Navigating Medicare Supplement Plans: Do You Need Medigap?

Medicare provides essential health coverage for millions of Americans aged 65 and older and younger individuals with disabilities. While Medicare covers a broad range of services, it doesn’t cover everything. That’s where Medicare Supplement Insurance, also known as Medigap, comes into play. This guide will help you understand Medigap plans, who needs them, and how to choose the right one for your needs.

What is Medigap?

Medigap is a type of private health insurance designed to supplement Original Medicare (Parts A and B). These policies help cover out-of-pocket costs that Medicare doesn’t pay for, such as:

- Deductibles

- Copayments

- Coinsurance

With Medigap, you can better predict your healthcare expenses and avoid hefty out-of-pocket costs when medical needs arise.

How Does Medigap Work?

- Medicare Pays First: When you receive healthcare services, Medicare covers its share of the approved amount.

- Medigap Pays Second: Your Medigap policy covers additional costs, depending on your plan.

Medigap policies only work with Original Medicare, not Medicare Advantage Plans (Part C).

Why Consider Medigap?

- High Out-of-Pocket Costs: Without Medigap, you could face significant expenses for hospital stays, skilled nursing care, or other services not fully covered by Medicare.

- Freedom to Choose Providers: Medigap allows you to visit any healthcare provider that accepts Medicare, offering greater flexibility.

- Travel Coverage: Some Medigap plans provide emergency healthcare coverage when traveling outside the United States.

Who Needs Medigap?

Medigap isn’t for everyone. Consider it if:

- You have Original Medicare (not a Medicare Advantage Plan).

- You frequently use healthcare services and want to minimize unpredictable expenses.

- You plan to travel internationally and want coverage abroad.

- You value the freedom to see any Medicare-approved doctor or specialist without network restrictions.

Understanding Medigap Plans

Medigap policies are standardized in most states and labeled by letters (A, B, C, D, F, G, K, L, M, and N). Each plan offers a different level of coverage.

Popular Medigap Plans

- Plan F:

- Comprehensive coverage.

- Covers Part A and B deductibles, coinsurance, and excess charges.

- Not available to new Medicare enrollees after January 1, 2020.

2. Plan G:

- Similar to Plan F but doesn’t cover the Part B deductible.

- Popular among new enrollees.

3. Plan N:

- Lower premiums.

- Requires copayments for some services, such as office visits and emergency room care.

What’s Not Covered by Medigap?

- Prescription drugs (you’ll need a separate Part D plan).

- Long-term care.

- Vision, dental, or hearing aids.

How to Choose the Right Medigap Plan

- Assess Your Needs

- How often do you visit doctors or specialists?

- Do you have any chronic conditions?

- Do you travel frequently?

- Compare Costs

Medigap premiums vary by:- Community Rating: Same premium for everyone in the area, regardless of age.

- Issue-Age Rating: Premium based on your age when you purchase the policy.

- Attained-Age Rating: Premium increases as you age.

- Consider Your Budget

- Higher premiums typically mean fewer out-of-pocket costs.

- Lower premiums may result in more out-of-pocket expenses when you need care.

- Check Provider Options

- Verify that your preferred doctors and hospitals accept Medicare.

- Verify that your preferred doctors and hospitals accept Medicare.

- Understand Enrollment Rules

- Enroll during your Medigap Open Enrollment Period (six months starting the month you turn 65 and enroll in Medicare Part B).

- During this period, insurers cannot deny coverage based on pre-existing conditions.

How Much Does Medigap Cost?

Medigap premiums vary widely based on your location, age, and the plan you choose. On average, you can expect to pay:

- $100 to $300 per month for a Medigap policy, depending on coverage.

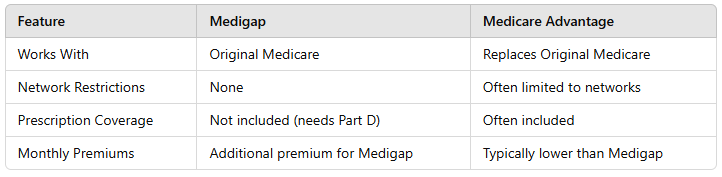

Medigap vs. Medicare Advantage: What’s the Difference?

While Medigap supplements Original Medicare, Medicare Advantage (Part C) is an alternative. Here’s how they differ:

Choose Medigap if you want predictable out-of-pocket costs and the freedom to choose any Medicare-approved provider. Opt for Medicare Advantage if you prefer lower premiums and don’t mind network restrictions.

Tips for Shopping for Medigap

- Research State Regulations:

- Medigap standardization rules may vary in Massachusetts, Minnesota, and Wisconsin.

- Compare Plans and Providers:

- Use Medicare’s official Plan Finder tool or consult a licensed insurance agent.

- Ask About Discounts:

- Some insurers offer discounts for nonsmokers, couples, or paying premiums annually.

- Read Reviews:

- Check the reputation of the insurance provider for customer service and claims handling.

- Reevaluate Periodically:

- Review your coverage needs annually during the Medicare Open Enrollment Period (October 15–December 7).

FAQs About Medigap

Q: Can I switch Medigap plans later?

A: You can switch, but you may face medical underwriting unless you have guaranteed issue rights.

Q: What happens if I drop my Medigap policy?

A: If you drop it and decide to re-enroll later, you may be subject to higher premiums or denial due to pre-existing conditions.

Q: Is Medigap necessary if I’m healthy?

A: Even if you’re healthy now, unexpected medical emergencies can result in significant costs. Medigap offers peace of mind.

Final Thoughts

Medigap plans provide valuable protection against the gaps in Original Medicare coverage, ensuring that unexpected medical expenses don’t derail your financial stability. By carefully evaluating your healthcare needs, budget, and travel plans, you can select the right Medigap policy for your circumstances.

Remember, your Medigap choice is a long-term investment in your health and peace of mind. Take the time to compare your options and consult a trusted insurance advisor to make an informed decision.

Read More Blog

Follow Us On:- Facebook